[ad_1]

The holiday season is upon us, but the stock market has made it difficult for many growth investors to feel joy this season. The main clues have been misleading; several actions in the Nasdaq composite hit 52-week lows as a select group of mega-caps backed the index with their high weightings.

But don’t be afraid; this is a time to be happy. The liquidation provided the opportunity to purchase shares of many high quality growth stocks at heavily discounted prices. Here are three stocks you’ll be glad you bought at these discounted prices.

Image source: Getty Images.

1. Meta-platforms

Technological holding Meta-platforms (NASDAQ: FB) has gone from its old name, Facebook, as a symbol of the company’s backbone of social media platforms to its focus on building the metaverse, where the physical and digital worlds meet.

The Metaverse has started to gain the attention of investors for its potentially significant growth prospects over the next decade, but Meta Platforms simply haven’t participated in the hype. The stock has remained stable for the past six months and has become cheaper than the S&P 500 in general.

FB PE report data by YCharts

Its price-to-earnings ratio is below 24, lower than that of the S&P 500, despite estimates calling for earnings per share (EPS) growth of 20% per year over the next three to five years, nearly double the historical growth rate. of the S&P 500 (a median of 11% per year).

But is it deserved? Meta owns some of the world’s most dominant social media platforms, including Facebook, Instagram, WhatsApp, and virtual reality hardware company Oculus. In its final quarter, the third quarter of 2021, more than 2.9 billion people used Meta’s various platforms.

This generates billions in advertising revenue and is very profitable. Revenue grew 35% year-over-year in the third quarter to $ 29 billion, including nearly $ 10 billion in free cash flow, adding to Meta’s $ 58 billion in cash flow. on its balance sheet. It invests billions in the development of its metaverse business while buying back more than $ 50 billion of its shares to turbocharge EPS at the same time.

Meta is a high quality company with financial data too strong for the stock to trade below the S&P 500. But here we are, so Meta is one of the best vacation deals out there.

2. CrowdStrike Holdings

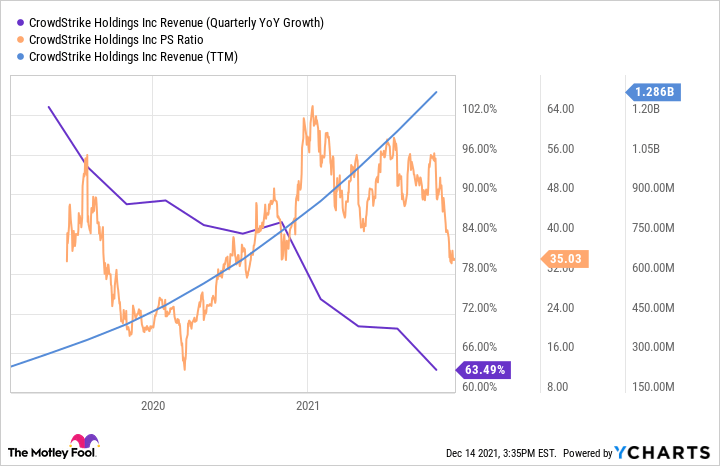

Cybersecurity company CrowdStrike Holdings (NASDAQ: CRWD) was one of the big winners of 2020 when the stock rose from around $ 40 per share during the March 2020 lows to nearly $ 300 per share earlier this year. Businesses appear in the news due to various hacks and breaches, and are now calling on companies like CrowdStrike to help defend themselves.

In the graph below, we can see how CrowdStrike quickly grew its revenue, but the share price surpassed that of the company, sending the price to sell ratio of the stock all the way to 64. It becomes the harder to sustain growth the bigger a business becomes, which is why we see the actual growth rate decrease over time. Certainly, a 63% growth is still very impressive.

Quarterly YoY Growth (CRWD) Revenue Data by YCharts

Investors could keep CrowdStrike on their radar as the valuation continues to decline. According to the research firm Gartner, the global endpoint cybersecurity market could be worth $ 21 billion by 2025, and Crowdstrike is a leader in this area. Businesses looking for cybersecurity solutions are likely to consider Crowdstrike given its good reputation.

The business is also profitable; its free cash flow grew at the same rate as its revenue (63%) in its third quarter of fiscal 2022, and its balance sheet has $ 1.9 billion in cash, so CrowdStrike is unlikely to have need to issue new shares to raise funds. Investors may invest in CrowdStrike on average because of its consistently high P / S ratio, but its strong fundamentals arguably at least warrant investors’ attention to this current downturn.

3. Roku

The streaming platform’s share price Roku (NASDAQ: ROKU) has fallen significantly from highs, down more than 50% since hitting $ 490 per share. The company’s software acts as an operating system for smart TVs; Roku also sells dongles that run streaming services on non-smart TVs.

Roku’s ownership on this platform has given it a lot of power over content creators and streaming service companies. Some companies have started to back down, including Alphabet recently, on the right to add YouTube to its platform. These competitive concerns spooked investors, pushing the stock to a P / S ratio of 12, close to pandemic lows. Roku and Alphabet recently reached a deal to expand the availability of YouTube on the Roku platform, stating that Roku’s platform is too important for YouTube to stray from.

ROKU PS ratio data by YCharts

Roku’s user base grew 23% year-over-year in the third quarter, to 56.4 million, and only gives Roku more influence the more users it gets. International markets could play an important role in Roku’s growth over the next few years. Roku has established itself as the premier streaming platform in Mexico, so it could experience similar success when it launches in Peru and Chile later this year. It was also recently launched in Germany.

In the United States alone, there are still 74 million homes paying for cable, so there is a lot of potential in these less developed markets, giving Roku a long-term growth avenue that is attractive over the course of time. of the currently depressed action.

This article represents the opinion of the author, who may disagree with the “official†recommendation position of a premium Motley Fool consulting service. We are motley! Challenging an investment thesis – even one of our own – helps us all to think critically about investing and make decisions that help us become smarter, happier, and richer.

[ad_2]

Comments are closed.