Join now for FREE unlimited access to Reuters.com

jetcityimage/iStock Editorial via Getty Images Many may be puzzled as to why we are taking opposing positions on Ford (NYSE:F) and Tesla (NASDAQ:TSLA); However, there is a significant disparity between the majority of automakers and Tesla due to the lifecycle of the industry and how investors value the respective stocks. This article covers Tesla’s outlook […]]]>

jetcityimage/iStock Editorial via Getty Images Many may be puzzled as to why we are taking opposing positions on Ford (NYSE:F) and Tesla (NASDAQ:TSLA); However, there is a significant disparity between the majority of automakers and Tesla due to the lifecycle of the industry and how investors value the respective stocks. This article covers Tesla’s outlook […]]]>jetcityimage/iStock Editorial via Getty Images

Many may be puzzled as to why we are taking opposing positions on Ford (NYSE:F) and Tesla (NASDAQ:TSLA); However, there is a significant disparity between the majority of automakers and Tesla due to the lifecycle of the industry and how investors value the respective stocks.

This article covers Tesla’s outlook given a surge in commodity prices. There has been a contentious debate where some have taken a stand and asserted that rising metal prices will increase variable costs and lead to less growth, while others argue that rising fossil fuel prices will trigger a buying spree for electric vehicles. This article takes a bird’s nest view and dissects both sides of the argument structurally and in reduced form.

I was quite surprised when I came across these measurements. I’ve analyzed the business segments of a few large companies over the course of my career, and we typically look at segment revenue and cash flow relative to CapEx while considering the level of CapEx relative to the past. I will, however, talk about Tesla’s company-wide metrics.

Tesla’s CapEx, which is its internal reinvestment rate, increased by 14.97x year-over-year as production ramps up, expansion into Texas with headquarters, factory expansion in Germany, and Chinese market penetration .

That being said, Tesla’s cash flow to CapEx has increased 3.4x over the past year, its Capex to revenue has improved by 62.80% and its operating margins improved 2.1 times. Keep in mind this was during a time of rising input costs.

It is also clear that Tesla management anticipated an increase in demand with an increase in finished products. You typically want to look at the entire pipeline of raw materials, work in progress, and finished goods and look for alignment when determining demand. It’s obviously an internal way of looking at things, but it gives substance.

Tesla 10-K

Finally, for this section, I would like to provide an overview of business expansion in China. Although Tesla’s sales in China fell by 5.6% month-over-month for February, it still produced 200% year-over-year growth, suggesting it is entering a robust consumer market with a vengeance. It is critical for a business to grow globally when it is susceptible to sales volatility; in effect, it allows it to no longer rely on the health of a single geographic consumer base and, in turn, to reduce the risks associated with the outlook for its stock. I see huge benefits for Tesla’s expansion into an economy with a huge GDP to say the least.

Much has been made of the commodity price spike and its impact on Tesla shares. While this will impact the company’s variable cost, I don’t think it will have a massive impact on its share price.

Historically speaking, Tesla investors didn’t hesitate much when metal and mineral prices rose, in fact there was a positive correlation.

Why could this be? Well, the stock market is looking forward and probably separating Tesla’s hypergrowth model from transient/highly elastic inflation. Don’t get me wrong, I think rising metal prices will have a massive impact on many auto stocks, but Tesla’s “best in class” status could prevent it from being correlated with other auto stocks. .

Additionally, Tesla’s status is still that of a Veblen product that serves a niche market, allowing its sales to be less susceptible to negative macroeconomic factors than more traditional automakers. Many analysts have argued that rising fossil fuel prices are a reason consumers are turning to electric vehicles. I think this is invalid because I don’t see how the masses would refinance a new vehicle when they are already financially stressed in the first place. Moreover, non-core inflation is more elastic than core inflation; most people who can finance vehicles have enough life experience to know that energy prices will trade in equilibrium over the lifetime of their car ownership (assuming they don’t change in any way maniacal). Thus, I see Tesla as a trend rather than its efficiency contributing to mass purchases; otherwise, we would have also seen the previous electric vehicles selling like hotcakes?

Bloomberg

To wrap up this section, I’d like to touch on a few macro factors. First, the commodity price spikes ex-post and in their current form have been mostly driven by push factors. I believe there was a massive overreaction during Covid-19 and subsequently with the Russian-Ukrainian conflict. I’m not saying in a linear way that commodity prices won’t be high for the foreseeable future, however, commodity prices tend to top in the short term and stay down in the long term, and that Won’t surprise me if traders soon overreact on the downside.

Let’s look at purchasing power and reopenings to provide a potential trade-off scenario.

First, consumer purchasing power has declined significantly over the past year, suggesting that we are likely to experience lower demand for industrial and precious metals in the near term, as they are directly tied to general consumption expenditure. To contextualize, you will only produce items at a rate that you expect consumers to buy, unless you are in a niche market like Tesla.

Second, we are seeing less stringent Covid policies. Reopenings will likely increase capacity for metal producers, which will likely contribute to price headwinds.

Our world in data

So, to sum up, I’m not implying that commodity prices will be cheap (relative to break-even point) over the next few years; however, I would argue that current price levels are overblown, and it’s clear that Tesla’s stock is forward-looking, meaning it’s unlikely to be as sensitive to transient commodity costs as it is. other industrial/consumer discretionary goods.

Many look to Tesla’s price/earnings ratio and its other price multiples to conclude that Tesla is overvalued, but that’s too simplistic a way to go about it. First, let’s justify the company’s PE.

Source: Alpha Research

Yes, Tesla’s PE ratio is outrageous, but if we look at its PE versus earnings growth, it’s actually still an undervalued metric. The PEG ratio has a value threshold of 1.00 and, in the case of Tesla, suggests that its earnings growth is currently outpacing its stock growth by about 3.85 times, leaving investors plenty of room to maneuver. to capture value.

The second argument is for an asset-based valuation, which gives us a fair value of $863.25. That in itself suggests the stock is undervalued based on past results, let alone future growth. If you see a stock trading at its current net asset value, you know it is valued by the market and trading rationally; however, Tesla is undervalued.

| Enterprise Value (EV) | $880.34 billion |

| Cash (NYSE:C) | $17.71 billion |

| Market value of debt (NYSE:D) | $8.90B |

| Outstanding shares (NYSE: N/A) | 1.03 million |

| The formula | (EV – D + C)/SO |

Source: Alpha Research

Although I have argued that rising commodity prices will not have a massive effect on Tesla stock, there is still a need to discuss the risks associated with it. I’m going to skip the obvious of rising variable costs, and I’m going to address hedging activities. To our knowledge, Tesla is not hedged against commodity prices, and that’s a bit of a rookie mistake; as a manufacturer, you would always want to hedge against input costs. I don’t know if Tesla has initiated any hedges since publishing its 10-K report in February. However, failure to do so could harm the effectiveness of the company’s financial management.

Also, from a stock perspective, Tesla has a worse Sharpe ratio than last year. The Sharpe ratio is a function of expected return relative to overall market volatility.

Why should this matter? Because you are essentially invested in a risky asset that does not justify the returns as well as in the past, therefore switching to an investment with more positively biased returns could be a valid option.

Tesla shares have a history of fending off rising input costs. The company has produced robust growth efficiently over the past year, which has also driven prices higher. Its expansion into China bodes well, given that it is less dependent on a single economy. The stock is also still undervalued, contrary to popular opinion.

We remain bullish on Tesla despite rising input costs.

AMC stock rose slightly on Tuesday amid renewed optimism on the Russian-Ukrainian front. AMC Entertainment had hoped for a rebound on the back of a strong Batman box office. Shares of the movie giant are expected to rebound on Tuesday as yields at risk. Update: AMC Holdings is trading at $15.66, up 2.96% in the […]]]>

AMC stock rose slightly on Tuesday amid renewed optimism on the Russian-Ukrainian front. AMC Entertainment had hoped for a rebound on the back of a strong Batman box office. Shares of the movie giant are expected to rebound on Tuesday as yields at risk. Update: AMC Holdings is trading at $15.66, up 2.96% in the […]]]>Update: AMC Holdings is trading at $15.66, up 2.96% in the last hour of trading, as Wall Street managed to turn green following some bullish headlines from the Russian-Ukrainian front . Humanitarian corridors were opened on Tuesday for cities such as Sumy and Mariupol. Also, Russia announced another corridor for Wednesday, which will allow the evacuation of Kiev, Kharkiv and other cities. But the headline that spurred the latest surge in risk appetite came from Ukraine, as the country declared it would no longer seek NATO membership.

It’s hard to predict how things will continue from now on, because if war-related worries eased further, attention would shift back to rising inflationary pressures and central bank responses to them. The United States will release February inflation figures next Thursday, and the annual figure is expected to have hit 7.8%, a multi-decade high. Meanwhile, falling demand for security has pushed government bond yields higher, with that of the 10-year US Treasury note currently at 1.87%, up twelve basis points in the daytime.

Previous Update: Holy Purse, Batman! AMC Holdings stock fell short of its third-best opening weekend since the start of the COVID-19 pandemic. Shares of the popular cinema chain fell 5.5% in the first half hour of trading on Tuesday, but recovered to -0.5% after an hour of trading. AMC stock is trading at nearly $15 per share. Again, the Nasdaq is having another bad session and is down 0.8% right now after Monday’s 3% drop. Over four million tickets were sold last weekend for AMC’s latest hit The Batman. The Caped Crusader movie grossed some $258 million from Thursday to Sunday. In the United States, AMC said it achieved an above-normal market share of 29% over the weekend.

AMC stock gave up some premarket gains as the market declines. Previously, European markets had been strong thanks to a joint debt issuance proposal, but now things are turning bearish again. AMC CEO Adam Aron said Monday night that using cryptocurrency is good for AMC Entertainment and that the company may consider launching its own crypto in the future if things go well. . He also said that they would stay very far on the right side of the law when it comes to crypto regulation. AMC shares are now trading at $14.96 for a loss of 1.7%. Previously, AMC shares were up more than 1% in Tuesday’s premarket.

AMC stock fell sharply on Monday as investors continued to exit high-risk names as oil soared and commodity prices remained in orbit. The outlook for the global economy has deteriorated significantly and high-growth stocks such as AMC have taken a disproportionate hit. In the current environment, any highly leveraged security will take a bigger hit as interest rates are expected to rise, but growth is expected to slow. A US recession is approaching as the US yield curve is dangerously close to turning negative.

See Wake Up Wall Street for everything you need to know before the stock market opens.

Investors, AMC traders – or monkeys as they like to be called – started Monday in high spirits as weekend box office numbers for Batman proved encouraging. However, AMC traders couldn’t stem the global bearish tide, and the stock was well beaten at the end of Monday. AMC stock closed at $15.21 for a loss of 8.2%. But Tuesday brings slightly more encouraging signs with slightly more optimistic tones of Russian demands on Ukraine, which has allowed risk assets to recover some ground. We would again expect a disproportionate rebound this time for AMC, and the stock should see a healthy gain at the open on Tuesday. We doubt this will hold for much longer than a few days as the overall sentiment remains bearish.

AMC is bearish below $21.04 and is likely to remain in a long-term downtrend. The goal is to get back below $10. $14.54 is the next key support. A breakout will likely cause AMC stock to accelerate lower.

AMC stock chart, daily

Tuesday should see a recovery in risk sentiment. We are already noticing that safe-haven buying of bonds and dollars has faded and everything has weakened on Tuesday. This should see higher risk assets. The first step is to hold $14.54. This prepares the day for a green day. $16.62 is the next level to target for AMC and finds resistance against Friday’s volume profile. Once above $17.20, volume eases, meaning a breakout to the $18 test is possible. $18.20 is strong resistance and will be hard to break.

AMC 15 minute chart

Previous update: AMC stock gave up some premarket gains as the market declines. Previously, European markets had been strong thanks to a joint debt issuance proposal, but now things are turning bearish again. AMC CEO Adam Aron said Monday night that using cryptocurrency is good for AMC Entertainment and that the company may consider launching its own crypto in the future if things go well. . He also said that they would stay very far on the right side of the law when it comes to crypto regulation. AMC shares are now trading at $14.96 for a loss of 1.7%. Previously, AMC shares rose more than 1% in Tuesday’s premarket.

Food for thought in light of the biggest stock market bubble in the United States. By Wolf Richter for WOLF STREET. Major European stock indices have plunged below their bubble highs of more than two decades ago. That don’t mean they dived this a lot this week, but that they had finally surpassed their previous […]]]>

Food for thought in light of the biggest stock market bubble in the United States. By Wolf Richter for WOLF STREET. Major European stock indices have plunged below their bubble highs of more than two decades ago. That don’t mean they dived this a lot this week, but that they had finally surpassed their previous […]]]>Major European stock indices have plunged below their bubble highs of more than two decades ago. That don’t mean they dived this a lot this week, but that they had finally surpassed their previous bubble highs of more than two decades ago, fueled by money printing, and then they plunged.

German stocks. The most quoted German stock index, the DAX, is a total return index that includes dividends and is therefore not comparable to a price index such as the S&P 500 index, which does not include dividends. But the less often cited DAX Kursindex (DAXK) is a price index and does not include dividends, and is comparable to the S&P 500 Index and most other major equity indices. So that’s what we’re going to use here.

The DAXK plunged 4.4% on Friday, and 10.1% for the week, to 5,517. Since the all-time closing high of 6,873 on January 5, 2021, it has plunged 19.7%. But wait… that all-time closing high was only up 10% from the March 2000 bubble peak – yes, that bubble that imploded 22 years ago. And on Friday, the index closed 11% below the peak of the March 2000 bubble. Note the gigantic volatility that investors have gone through over these 22 years to find themselves below where they started.

UK stocks. Britain’s FTSE 100 price index fell 3.5% on Friday and 6.7% for the week to 6,987. The index is now down 10% from its all-time high in May 2018 But wait… Friday’s close is slightly down from the December 31, 1999 close, which was the bubble high 22 years ago, and now the index is back:

French stocks. The CAC 40 price index plunged 5.0% on Friday and 10.2% for the week, to 6,062, and is down 18% from its all-time high in January 2021. But wait …yes, the index has now fallen 12% below its bubble high in September 2000. And note the horrible volatility investors have had to endure to get nowhere:

Spanish stocks. Spain’s IBEX 35 index fell 3.6% on Friday and 9.0% for the week to 7,721, and yes, for buyers and holders, this stock market has been a total 25-year nightmare. On Friday, stocks fell to the lower end of the 25-year range, to a level already seen in 1998. The index is now down 52% from its peak in December 2007:

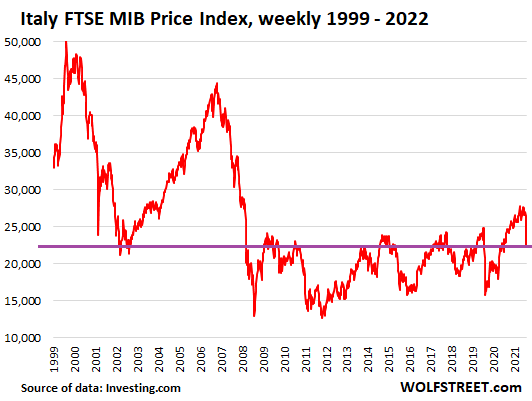

Italian stocks. Italy’s FTSE MIB index plunged 6.2% on Friday and 12.8% for the week. This horror show is now down 55% from the March 2000 peak, and back to where it was in the 1990s – as my data only goes back to December 1997, and even then, l he index was even higher than today. Another great market for buyers and holders to eliminate:

There are a bunch of other stock indices around the world, including big indices like the Japanese Nikkei 225 and China’s Shanghai Stock Exchange, which are now below their bubble levels from a very long time ago. many years.

This shows that for many major stock markets around the world, buy and hold only works if you buy low and hold until prices are high, then sell before they dip again. So basic market timing. Otherwise, you could be screwed for decades, or possibly the rest of your life – the Nikkei is still down 33% from that 1989 bubble peak. Once those mega-bubbles implode, the stock markets may not see their old highs for decades. Food for thought.

Do you like to read WOLF STREET and want to support it? You use ad blockers – I completely understand why – but you want to support the site? You can donate. I greatly appreciate it. Click on the mug of beer and iced tea to find out how:

Would you like to be notified by e-mail when WOLF STREET publishes a new article? Register here.

![]()

/cloudfront-us-east-2.images.arcpublishing.com/reuters/6N4HEO75CBNH3NFWRKCYE2COXM.jpg) Russian ruble coins are seen in front of the US dollar banknote displayed in this illustration taken February 24, 2022. REUTERS/Dado Ruvic/Illustration/Files Join now for FREE unlimited access to Reuters.com Register NEW YORK, March 2 (Reuters) – The ruble hit a new high of 110 to the dollar in Moscow on Wednesday and fell back […]]]>

Russian ruble coins are seen in front of the US dollar banknote displayed in this illustration taken February 24, 2022. REUTERS/Dado Ruvic/Illustration/Files Join now for FREE unlimited access to Reuters.com Register NEW YORK, March 2 (Reuters) – The ruble hit a new high of 110 to the dollar in Moscow on Wednesday and fell back […]]]>Russian ruble coins are seen in front of the US dollar banknote displayed in this illustration taken February 24, 2022. REUTERS/Dado Ruvic/Illustration/Files

NEW YORK, March 2 (Reuters) – The ruble hit a new high of 110 to the dollar in Moscow on Wednesday and fell back below 100 in other trading venues, though it remained under pressure as the country’s financial system reeled under the weight of Western sanctions imposed following Moscow’s invasion of Ukraine.

The Russian stock market remained closed and bond trading showed wide bid-ask spreads and low volume.

The ruble fell 4.5% to 106.02 against the dollar in Moscow trade, earlier hitting 110.0, a record low. It has lost about a third of its value against the dollar since the start of the year. Against the euro, it lost 2.5% to end the day at 115.40.

But trade out of Russia saw the currency gain almost 10% on the day towards 95 per dollar, still 20% lower than where it traded in the first half of February.

“Ruble volatility remains extremely high, which could be caused by unstable currency sales by exporters as well as further heightened stress levels among market participants and households in particular,” Raiffeisen said in a statement. note.

Russia responded to the weak currency by more than doubling interest rates to 20% and telling businesses to convert 80% of their earnings into foreign currency domestically because the central bank, or CBR, which is now under Western sanctions, halted exchange interventions.

The weak ruble will affect living standards in Russia and stoke already high inflation, while Western sanctions are expected to create shortages of essential goods and services such as cars or flights. Read more

Many international companies have announced plans to leave Russia as the country’s credit ratings come under pressure due to the crisis.

Credit rating agency Moody’s said it was reviewing Russia’s rating for a downgrade, a move that “reflects the negative credit implications for Russia’s credit profile of additional and tougher sanctions. imposed”.

Meanwhile, Scope Ratings said the capital controls “raise important questions about the Russian state’s willingness to repay its debt to foreign residents” after it downgraded its rating to junk status.

The measures, Scope added, make Russia “more vulnerable to banking and liquidity crises.”

JPMorgan said a deep recession was brewing for Russia and the bank was reassessing its regional macroeconomic forecast.

“The most recent actions targeting CBR are a complete game-changer,” JPMorgan said.

“Russia’s large current account surplus could have accommodated large capital outflows, but with accompanying CBR and SWIFT sanctions, in addition to existing restrictions, it is likely that Russia’s export earnings Russia will be disrupted and capital outflows will likely be immediate.”

Several Russian banks have been excluded from the SWIFT global financial network which facilitates transfers between banks.

As Russian households and businesses rushed to convert the falling ruble into foreign currency, banks raised foreign currency deposit rates to attract those flows.

Russia’s biggest lender, Sberbank (SBER.MM), offers to pay 4% on deposits up to $1,000, while the biggest private lender, Alfa Bank, offers 8% on three-dollar deposits. month. For deposits in rubles, Sberbank offers an annual return of 20%.

Sberbank said on Wednesday it was quitting almost all European markets, blaming large cash outflows and threats to its staff and property, after the ECB ordered the closure of its European branch. Read more

The bank’s London-traded shares fell to 4.5 cents from $16 at the start of the year.

A U.S.-traded ETF of Russian companies and others with high Russian exposure fell nearly 8% on Wednesday, down 70% since mid-February.

Moscow calls its actions in Ukraine a “special operation” which it says is not designed to occupy territory but to destroy the military capabilities of its southern neighbor and capture what it sees as dangerous nationalists.

Reuters reporting; Editing by Andrew Heavens, Edmund Blair, Jane Merriman and Jonathan Oatis

Our standards: The Thomson Reuters Trust Principles.

CAMBRIDGE, Mass. – Russia’s invasion of Ukraine was swift and dramatic, but the economic consequences will be much slower to materialize and less dramatic. The war itself is extremely tragic, first and foremost for the Ukrainian people, but also for the Russian people and the world order in general. When something like this happens, we […]]]>

CAMBRIDGE, Mass. – Russia’s invasion of Ukraine was swift and dramatic, but the economic consequences will be much slower to materialize and less dramatic. The war itself is extremely tragic, first and foremost for the Ukrainian people, but also for the Russian people and the world order in general. When something like this happens, we […]]]>CAMBRIDGE, Mass. – Russia’s invasion of Ukraine was swift and dramatic, but the economic consequences will be much slower to materialize and less dramatic.

The war itself is extremely tragic, first and foremost for the Ukrainian people, but also for the Russian people and the world order in general. When something like this happens, we expect it to be like a morality play in which all the bad consequences happen equally dramatically across all dimensions, including the economy. But the economy doesn’t work that way.

Admittedly, the financial markets reacted quickly to the announcement of the Russian invasion. The MSCI All Country World Index, a leading indicator of global equities, fell to its lowest level in nearly a year. The price of oil rose above $100 a barrel, while natural gas prices in Europe initially jumped nearly 70%.

These increases in energy prices will have a negative effect on the global economy. Europe is particularly vulnerable, as it has done little in recent years to reduce its dependence on Russian gas, and in some cases, notably Germany, which has abandoned nuclear, it has even exacerbated it.

Oil-importing countries will be penalized by rising prices. The United States is more hedged: because its oil production equals its oil consumption, more expensive oil is roughly neutral for gross domestic product. But rising oil prices will hurt American consumers while helping a more limited segment of businesses and workers tied to the oil and gas industry. Soaring prices will also add to inflation, which is already at its highest level in a generation in the United States, Europe and other advanced economies.

But it is necessary to take a step back from these immediate consequences. At $100 a barrel, oil is about a quarter below its inflation-adjusted price between 2011 and 2014. Additionally, oil futures prices are below spot prices, suggesting that the market expects this increase to be temporary. Central banks could therefore largely weather events in Ukraine, neither delaying the tightening nor accelerating it in response to rising headline inflation. And global stock markets are still up over the past year.

Likewise, although the Russian stock market has fallen significantly since the start of the invasion, Western sanctions are unlikely to have immediate dramatic effects. Sanctions rarely do this; they are simply not the economic equivalent of the bombs that Russia is currently dropping on Ukraine.

Moreover, Russia is better prepared than most countries to face sanctions. The country ran a huge current account surplus and accumulated record foreign exchange reserves of $630 billion, enough to cover nearly two years of imports. And while Russia depends on revenues from Europe, Europeans depend on Russian oil and gas – which may be even harder to replace in the short term.

But, in the longer term, Russia is likely to be the biggest economic loser from the conflict (after Ukraine, whose losses will go well beyond what can be measured in national accounts). Russia’s economy and the well-being of its people have stagnated since the Kremlin annexed Crimea in 2014. The fallout from its current large-scale invasion will almost certainly be more severe over time. Sanctions will claim more and more victims, and Russia’s growing isolation, as well as heightened investor uncertainty, will weaken trade and other economic ties. In addition, Europe can be expected to reduce its dependence on fossil fuels vis-à-vis Russia.

The longer-term economic consequences for the rest of the world will be much less severe than they are for Russia, but they will remain a persistent challenge for policymakers. There is a risk, albeit relatively unlikely, that the rise in near-term inflation will become rooted in increasingly less anchored inflation expectations and therefore persist. If that happens, the already difficult job of central banks will become even more complicated.

In addition, defense budgets are expected to increase in Europe, the United States and some other countries to reflect the increasingly dangerous global situation. It won’t reduce GDP growth, but it will reduce people’s well-being, because resources dedicated to defense are resources that cannot be spent on consumption or investment in education, health or infrastructure.

The medium and long-term consequences for the global economy of Russia’s invasion of Ukraine will depend on the choices. By invading, Russia has already made a terrible choice. The United States, the European Union and other governments have made initial choices on sanctions, but it remains to be seen how Russia will react to them or if new sanctions will be imposed. As sanctions and counter-responses intensify, the costs will be greater – first and foremost for Russia, but also to some extent for the rest of the global economy.

Global economic relations are positive-sum, and Russia’s growing isolation will remove a small positive. More broadly, uncertainty is never good for the economy.

But, as the world continues to react to the Russian invasion, worries about GDP seem small by comparison. Much more important is a world where people and countries feel safe. And it’s something worth paying for – even more than world leaders have paid so far.

Jason Furman, former Chairman of President Barack Obama’s Council of Economic Advisers, is a Professor of Economic Policy Practice at Harvard University’s John F. Kennedy School of Government and a Senior Fellow at the Peterson Institute for International Economics. © Syndicate Project, 2022

In an age of both misinformation and too much information, quality journalism is more crucial than ever.

By subscribing, you can help us tell the story well.

SUBSCRIBE NOW

GlobeNewswire2022-02-26 ORO VALLEY, Ariz., Feb. 25 12, 2022 (GLOBE NEWSWIRE) — Tautachrome Inc. (OTC: TTCM) today outlines the direction and focus of its Integrity Defense activity aimed at combating the criminality of stock market trolls targeting the company’s securities. The Company understands that there are internet platforms of all kinds that allow anyone to talk […]]]>

GlobeNewswire2022-02-26 ORO VALLEY, Ariz., Feb. 25 12, 2022 (GLOBE NEWSWIRE) — Tautachrome Inc. (OTC: TTCM) today outlines the direction and focus of its Integrity Defense activity aimed at combating the criminality of stock market trolls targeting the company’s securities. The Company understands that there are internet platforms of all kinds that allow anyone to talk […]]]>ORO VALLEY, Ariz., Feb. 25 12, 2022 (GLOBE NEWSWIRE) — Tautachrome Inc. (OTC: TTCM) today outlines the direction and focus of its Integrity Defense activity aimed at combating the criminality of stock market trolls targeting the company’s securities.

The Company understands that there are internet platforms of all kinds that allow anyone to talk or shout comments of any kind. And we consider that to be good. But we also believe that the power to comment does not include the right to criminally troll, that is, to hide behind pseudonyms and make false and misleading statements intended to harm others.

As we announced earlier this week, the company has implemented an integrity defense activity aimed at curbing stock market troll attacks on the company’s securities and has reactivated Michael Nugent, our former head of integrity. advancement, to direct the activity.

Mr. Nugent spoke today about the company’s direction and focus on this business.

“For a public company like Tautachrome, trolling is serious business,” Nugent said. “We know from first-hand experience that trolls will use certain investment forums to make false and misleading statements for the express purpose of manipulating the price of the stocks they trade, which has the effect of stealing money. money in the accounts of other investors who are unaware of the manipulation.

Nugent went on to say, “Criminal trolling increases exponentially when owners of investment forums not only allow such trolling, but go out of their way to protect trolls from exposure. InvestorsHub is an example of an investment forum whose policies protect stock trolling. We witness the trolling of our own business by pseudonymous individuals on this forum, and find the forum’s reluctance to act to remedy the illegal behavior very troubling. »

“My information shows,” he said, “that InvestorsHub is a wholly-owned subsidiary of London-based ADVFN PLC, whose CEO, Clem Chambers, has for years been responsible for the forum’s reluctance to curb fishing. criminal trolling on their InvestorsHub. Chambers allowed pseudonymous trolls to post false and misleading information about publicly traded companies to gain visits and clicks to sell advertising, yet carefully shielded his own company, ADVFN PLC, from such a troll attack. .

“Today we learned,” Nugent said, “that Chambers was removed from ADVFN PLC yesterday and replaced by new CEO, Mr. Jonathan Mullins. This could be good news for the integrity of the InvestorsHub forum. So today, we’re calling on Mr. Mullins to tear down the wall that InvestorsHub has erected to protect criminal trolls.

The Society intends to adapt to the changes that come our way and we fully understand that the public environment is constantly changing. But the securities laws we follow are stable and don’t change that way. They need to be enforced so that criminal trolls are held accountable.

About Tautachrome, Inc: Tautachrome, Inc. (OTC: TTCM) is an emerging, growing Internet applications company. The company has licenses, patents and patents pending in the areas of augmented reality, smartphone image authentication and image-based social networking. The company leverages these technologies to develop privacy and security-based applications for business and personal use globally.

Tautachrome, Inc. posts important information and updates via tweets from the company’s official Twitter page https://twitter.com/Tautachrome

Forward-looking statements: Statements made in this press release are forward-looking and are made pursuant to the safe harbor provisions of the Securities Litigation Reform Act of 1995. Risk factors that could cause actual results to differ materially from those projected in the forward-looking statements include, but but not limited to, general business conditions, risks of raising sufficient funds to achieve the Company’s objectives, growth management risks, government regulatory risks, technology development risks, risks of delay in timing and political and other business risks. All forward-looking statements are expressly qualified in their entirety by this paragraph and the risks and other factors detailed in Tautachrome’s reports filed with the Securities and Exchange Commission. Tautachrome undertakes no obligation to update these forward-looking statements.

Press and investor contact:

David LaMountain, COO

520-318-5578

[email protected]

The story continues under the ad What is happening here? The city has over half a billion dollars burning a hole in its pocket but failing to meet the basic needs of its most vulnerable residents. This approach is wrong, causes traumatic suffering and weakens the social fabric of our city. City leaders may ask […]]]>

The story continues under the ad What is happening here? The city has over half a billion dollars burning a hole in its pocket but failing to meet the basic needs of its most vulnerable residents. This approach is wrong, causes traumatic suffering and weakens the social fabric of our city. City leaders may ask […]]]>What is happening here? The city has over half a billion dollars burning a hole in its pocket but failing to meet the basic needs of its most vulnerable residents. This approach is wrong, causes traumatic suffering and weakens the social fabric of our city. City leaders may ask us to be understanding of their budget decisions, but with such surpluses we rightly feel angry and disappointed with their choices.

For less than $200 million, the mayor could protect these households from the cascade of damage to health, stability and security that evictions and homelessness bring. Our low-income black and brown neighbors — many of them are the famous “essential workers” of the pandemic and the dc economy motor — have been suffering for nearly two years now, as white neighbors with far greater resources have recovered and even increased their wealth.

Bowser must rush to meet critical and urgent needs for rent and utilities, dedicating a portion of the surplus to preventing evictions and utility cuts. Although DC did not receive the $187 million the mayor requested from the federal government for these purposes, it can now use the excess funds to fill the overburdened Emergency Rental Assistance Program and provide assistance. emergency in terms of public services and the Internet. It can also increase funding for the rapid rehousing program to ensure the stability of these families. As we emerge from the pandemic, with our huge budget surplus, not a single resident should face eviction or homelessness due to economic hardship.

Why act now? Aid cannot wait for the regular budget process. By late spring, tens of thousands of renters will potentially be facing eviction, with the average DC household facing an eviction claim for less than the cost of a area median monthly rent.

If the $1.5 billion surpluses of the last three years tell us anything, it is that we need to be less careful in our budgeting and put human needs first. Many of these households would not be in dire straits if we had allocated funds more generously for critical pandemic relief through the normal budget process. We budgeted for savings when we had to meet the real level of need with the resources we clearly had.

While recent stock market jitters and inflation may shake our collective nerves, the accumulation of wealth at the top has exploded during the pandemic. It is still essential for the Mayor, the DC Council and all of us to remember that preventing homelessness and evictions is the right path and costs only a fraction of what it will take to deal with the consequences later. . The costs can be measured in dollars, wasted human potential, and long-term adverse effects on health, learning, and productivity.

Bowser should immediately tap into the surplus to help avert an eviction crisis. She and the DC Council must not take the “cautious, let’s see” approach to budgeting that prioritized wealth over community well-being. We have literally made savings more important than well-being. We have to make a different choice in the future.

Time for a raid. The Russian invasion of Ukraine has caused turmoil on the ground and in financial markets. This triggered a sell-off in global equity markets. Prices for oil and natural gas and other commodities such as wheat, as well as gold, palladium and other precious metals jumped as investors feared supply disruptions. They […]]]>

Time for a raid. The Russian invasion of Ukraine has caused turmoil on the ground and in financial markets. This triggered a sell-off in global equity markets. Prices for oil and natural gas and other commodities such as wheat, as well as gold, palladium and other precious metals jumped as investors feared supply disruptions. They […]]]>Time for a raid.

The Russian invasion of Ukraine has caused turmoil on the ground and in financial markets. This triggered a sell-off in global equity markets. Prices for oil and natural gas and other commodities such as wheat, as well as gold, palladium and other precious metals jumped as investors feared supply disruptions.

They piled into gold, European and US government bonds, which are seen as safer investments in times of trouble. Russian assets sold off, from the ruble to stocks and bonds.

UK and European stock indices fell between 3% (FTSE 100 index) and 5% (German stock market).

Crude Brentthe global oil benchmark, rose above $105 a barrel for the first time since August 2014. It now stands at $104.50 a barrel, up almost 8%.

British gas for next day delivery jumped 40% to £280 per therm.

European wheat futures jumped 20% to a record price of €344 a tonne, the biggest rise in nine years. Ukraine is the fifth largest wheat exporter in the world and considered the breadbasket of Europe. This does not bode well for consumers – food and energy prices are already high.

Gold and the prices of other precious metals, including palladium, platinum and nickel, have surged. Spot gold gained more than 3% today to $1,969 an ounce. Aluminum reached a record of $3,443 per ton in London.

The Russian Ruble hit a record low of 80.60 to the dollar, but then recovered somewhat to 83.4, still down 2.7% on the day, after the Bank of Russia said it would intervene to strengthen the currency. The ruble is trading at 93.7 per euro, down 2.2%.

Russian stocks fell 50% when trading resumed on the Moscow Stock Exchange. The dollar-denominated RTS index fell 49.93% in early trading and then traded down 34%. The ruble-denominated Moex index fell 45% to 1,690.13, then 31%.

Listed in London Russian companies suffered sharp drops in share price, with Sberbank plunging 61% and Gazprom losing 28%.

As Russian public debt liquidated, yields on benchmark 10-year OFZ ruble bonds (which move inversely to prices) hit 10.93%, the highest since early 2016.

By Bill SchmickChronicler of the iBerkshires4:23 p.m. / Friday, February 18, 2022 Over the next three weeks, stocks will likely trade in a wide range. The caveat to this forecast: if the Fed suddenly changes policy, or if a deadly war breaks out in Ukraine. Those are two big ifs. Unfortunately, I can’t predict when […]]]>

By Bill SchmickChronicler of the iBerkshires4:23 p.m. / Friday, February 18, 2022 Over the next three weeks, stocks will likely trade in a wide range. The caveat to this forecast: if the Fed suddenly changes policy, or if a deadly war breaks out in Ukraine. Those are two big ifs. Unfortunately, I can’t predict when […]]]>

By Bill SchmickChronicler of the iBerkshires

|

Over the next three weeks, stocks will likely trade in a wide range. The caveat to this forecast: if the Fed suddenly changes policy, or if a deadly war breaks out in Ukraine. Those are two big ifs. Unfortunately, I can’t predict when or what the next Fed chief will say, or predict Vladimir Putin’s next move.

The next meeting of the Federal Open Market Committee will take place in mid-March. The latest CPI and PPI inflation data show that inflation is accelerating at a much faster pace than economists and the Fed expected. It is almost certain, according to bond market vigilantes, that the Federal Reserve Bank will raise interest rates at that time. So, the only question is whether the rate hike will be 25 or 50 basis points.

This will only be part of the equation. Investors will expect Chairman Jerome Powell to give them more information on how many rate hikes they can expect in the future, and what other monetary tightening the Fed is also planning. The risk will be that the stock market fades and tests the lows if the Fed is seen to be more hawkish on tightening than expected.

That in the meantime, we have something to occupy our attention. This week, market concerns about interest rates were supplanted by Russia’s intentions towards Ukraine. So far, the conflict has played out in the media in a “he said, she said” war of accusations and counter-accusations.

War is never a good thing, suffice it to say. But besides the human costs of such a conflict, there would also be an economic price to pay. The sanctions that the United States and its allies are prepared to impose on Russia in response to perceived aggression would cause damage to the global economy and to the United States as well.

Russia supplies a large part of the products that the rest of the world consumes. The sanctions could immediately cause major price spikes for commodities such as oil, gas and coal. Russia is also a major exporter of rare earth minerals and heavy metals. A third of the world’s supply of palladium (used in catalytic converters), for example, and titanium (think airplanes) is also mined and exported by Russia.

Ukraine is also a major source of neon, an essential input in the manufacture of semiconductors. Ukraine is one of the world’s largest producers of wheat, as well as fertilizer (just like Russia). Hostilities could harm their ability to export or even harvest the country’s wheat supply.

I would expect price spikes in several food items as a result. This would add fuel to the inflation fire and could force the Fed to become even more aggressive in raising interest rates. That wouldn’t be a pretty picture for stock market investors.

To be honest, no one knows if Russia is bluffing or serious about the invasion as the next step. For me, a telltale sign of their intent would be any movement of medical facilities and supplies to troop assembly areas and the border with Ukraine. This week I saw exactly that.

The risk is obvious. A shooting war would likely see the S&P 500 index retest the January 24 lows (4,222). Geopolitical events generally have a limited impact on the stock market unless hostilities are prolonged and wide-ranging. If, on the other hand, a negotiated settlement were to take place, markets would likely soar higher. That “if” word will keep investors nervous and prices in a box with each security capable of driving the markets up or down 1-2%.

Anyone wishing to obtain personalized investment advice should contact a qualified investment adviser. None of the information presented in this article is intended to be and should not be construed as an endorsement by OPI, Inc. or a solicitation to become a customer of OPI. The reader should not assume that the specific strategies or investments discussed are employed, purchased, sold or owned by OPI. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or capital. This communication may include opinions and forward-looking statements, and we cannot guarantee that these beliefs and expectations will prove to be accurate. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or capital. This communication may include opinions and forward-looking statements, and we cannot guarantee that these beliefs and expectations will prove to be accurate.

This year, markets are placing risk in the “risk premium”. Any asset that typically pays more than a low-risk (or zero-return) bond will expose you to losses from time to time. But that’s the problem: risk is the cost of potentially higher gains. Some investors take on more risk than others. If you’re facing bigger […]]]>

This year, markets are placing risk in the “risk premium”. Any asset that typically pays more than a low-risk (or zero-return) bond will expose you to losses from time to time. But that’s the problem: risk is the cost of potentially higher gains. Some investors take on more risk than others. If you’re facing bigger […]]]>This year, markets are placing risk in the “risk premium”. Any asset that typically pays more than a low-risk (or zero-return) bond will expose you to losses from time to time. But that’s the problem: risk is the cost of potentially higher gains. Some investors take on more risk than others. If you’re facing bigger losses than you can afford and you’re not getting a higher overall return, rethink your investment strategy. As volatility returns and the era of memestocks comes to an end, it’s worth asking: Should retail investors even be allowed to own individual stocks?

This may seem extreme. After all, what epitomizes capitalism better than buying a piece of a company you admire, respect, or just think will make you rich? Except that we put safeguards in place when it comes to other aspects of our lives, from data protection to buying a mattress. Yet risk taking, the essence of individual stock investing, is not only unlimited, it is often encouraged.

Let us distinguish between owning shares and owning shares in particular corporations. We should encourage share ownership. Portfolio risk is often the only way to grow wealth. But there is a good way to take risks and a not so good one.

Between the rise of online trading platforms and [retirement plans], more people own stocks than ever before, but we never bothered to educate people on the basics. When you invest in the stock market, you face two types of risk: idiosyncratic, or the risk that a single stock will fall; and systematic, the risk that the whole market will go down. There is not much you can do about this last risk except reduce your exposure and give up some potential returns. But idiosyncratic risk is avoidable; you just need to buy lots and lots of other stocks that make up for a stock’s losses. If you diversify properly, you get the only free lunch in finance: higher expected returns and less risk. And the cheapest and easiest way to get that perfect diversification is to buy an index fund with hundreds or thousands of stocks. This partly explains why index funds tend to outperform hand-picked stock portfolios.

During America’s memestock frenzy, it was surreal to see consumer welfare advocate Senator Elizabeth Warren arguing that the problem wasn’t small day traders, it was big investor behavior that needed to be curbed. to make market speculation fair for all. But whatever regulators do, stock market speculation is rarely good for retail investors. Especially when betting against institutional investors, who often just have a natural advantage due to their much bigger pockets, time and arguably greater skills.

While there are good reasons not to own individual stocks, there is a social benefit to this practice. Ownership connects people to companies, educates investors about the markets, and gets people thinking about how they work, which can help them feel better about capitalism, which is important in these times.

Ideally, retail investors should treat stock picking as a hobby, not an investment, and devote only a small portion of their portfolio to individual stocks. Just as you don’t go to the casino as an investment strategy, but for certain entertainment, so should buying specific stocks.

And yet, from seatbelts to vaccinations, governments can’t always rely on citizens to do what’s in their own best interests. They need a little help. For argument’s sake, here are a few options:

First, let only accredited investors, high net worth individuals and hedge funds buy individual stocks. This is how it already works for private assets. The system needs someone to buy and sell individual stocks for price discovery and to maintain market efficiency, but eligible investors might be limited to those best suited for this role. While that might be okay in a world of pure financial theory, it’s probably not good for society.

Second, it is harder to own individual stocks. Buying stocks is incredibly easy. Unlike pension plans, which warn us of the consequences of a withdrawal, no such warning is sent before we take inventory action. Perhaps we should at the very least be forced to take similar steps, with similar precautions, to buy individual stocks. This may not make a difference to most buyers, but it at least tries to educate people that investing in individual stocks comes with additional risk and shouldn’t be the norm.

Three, keep doing what we’re doing. Facilitate individual trading on different platforms and let a growing number of people bear inefficient risk. Some people will suffer financially, but that’s life.

The last option is the most likely. But the second would be best. I am normally skeptical of clumsy regulation and think [people] need more risk in their lives to thrive. But if regulation is supposed to do anything, it’s to incentivize people to take better risks while preserving as much choice as possible.

Allison Schrager is a columnist at Bloomberg Opinion, senior fellow at the Manhattan Institute, and author of “An Economist Walks Into a Brothel: And Other Unexpected Places to Understand Risk”

Never miss a story! Stay connected and informed with Mint. Download our app now!!

{kind=link}