jetcityimage/iStock Editorial via Getty Images Many may be puzzled as to why we are taking opposing positions on Ford (NYSE:F) and Tesla (NASDAQ:TSLA); However, there is a significant disparity between the majority of automakers and Tesla due to the lifecycle of the industry and how investors value the respective stocks. This article covers Tesla’s outlook […]]]>

jetcityimage/iStock Editorial via Getty Images Many may be puzzled as to why we are taking opposing positions on Ford (NYSE:F) and Tesla (NASDAQ:TSLA); However, there is a significant disparity between the majority of automakers and Tesla due to the lifecycle of the industry and how investors value the respective stocks. This article covers Tesla’s outlook […]]]>

It is one of the most popular real estate investment trusts (REITs) in the market today and pays a high yielding monthly dividend. It also operates in a sector poised for a serious rebound in the coming months. So maybe retail oriented Real estate income (NYSE:O)currently priced at just over $66 per share, may reach […]]]>

It is one of the most popular real estate investment trusts (REITs) in the market today and pays a high yielding monthly dividend. It also operates in a sector poised for a serious rebound in the coming months. So maybe retail oriented Real estate income (NYSE:O)currently priced at just over $66 per share, may reach […]]]> Image source: Getty Images Be sure to use your tax refund wisely. Key points Many Americans will receive a large tax refund this year. This lump sum payment represents a great opportunity to improve your finances. Paying off debt, building an emergency fund, and investing are some smart ways to use your tax refund. Many […]]]>

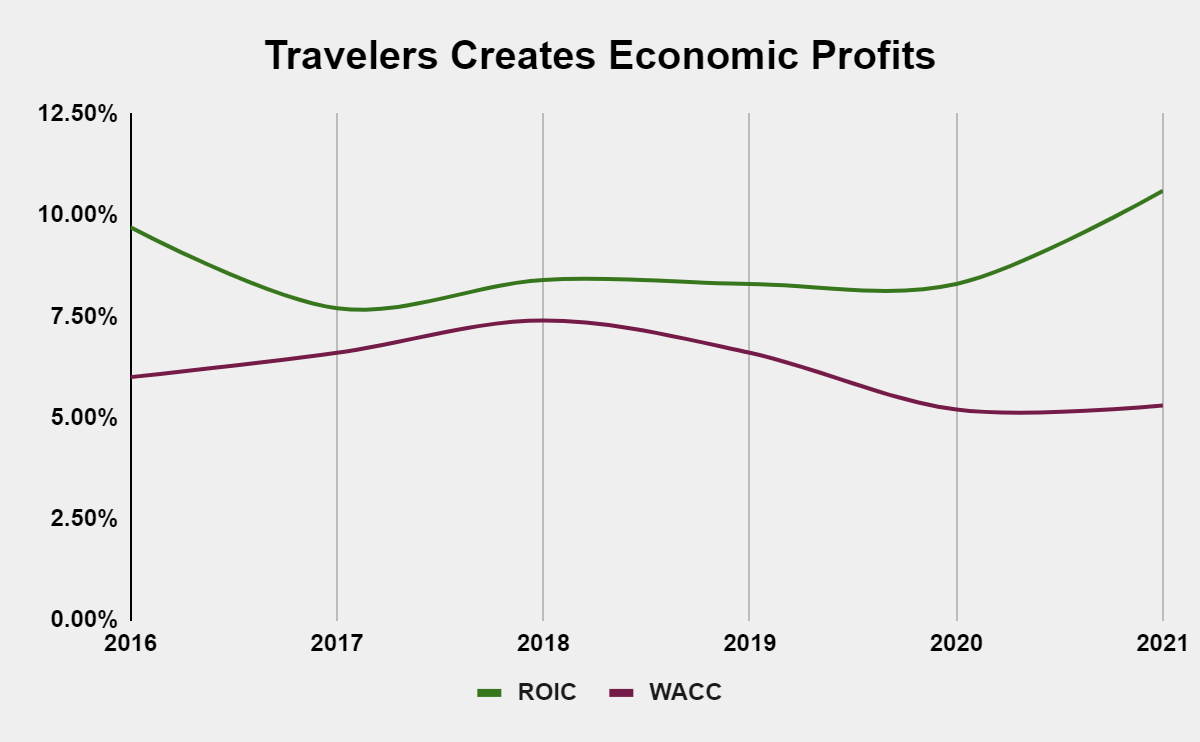

Image source: Getty Images Be sure to use your tax refund wisely. Key points Many Americans will receive a large tax refund this year. This lump sum payment represents a great opportunity to improve your finances. Paying off debt, building an emergency fund, and investing are some smart ways to use your tax refund. Many […]]]> Spencer Platt/Getty Images News The Travelers Companies, Inc. (NYSE:TRV) is one of the largest P&C insurance companies in the country. Although the P&C insurance industry is highly fragmented and competitive, its unique nature allows insurers to realize economic benefits. The industry has shown positive results despite struggling with a return from non-catastrophic losses to pre-pandemic […]]]>

Spencer Platt/Getty Images News The Travelers Companies, Inc. (NYSE:TRV) is one of the largest P&C insurance companies in the country. Although the P&C insurance industry is highly fragmented and competitive, its unique nature allows insurers to realize economic benefits. The industry has shown positive results despite struggling with a return from non-catastrophic losses to pre-pandemic […]]]>

LONDON, ENGLAND – AUGUST 09: In this photo illustration an image of the Google logo is reflected … [+] on the eye of a young man on August 09, 2017 in London, England. Founded in 1995 by Sergey Brin and Larry Page, Google today makes hundreds of products used by billions of people around the […]]]>

LONDON, ENGLAND – AUGUST 09: In this photo illustration an image of the Google logo is reflected … [+] on the eye of a young man on August 09, 2017 in London, England. Founded in 1995 by Sergey Brin and Larry Page, Google today makes hundreds of products used by billions of people around the […]]]> A new study from Boon Brokers has discovered that 83% of people across the country are unaware of certain activity on their bank statements, which could be a red flag for a mortgage lender. A survey of 2,863 UK residents conducted by TLF on behalf of the mortgage broker also found that 58% of respondents […]]]>

A new study from Boon Brokers has discovered that 83% of people across the country are unaware of certain activity on their bank statements, which could be a red flag for a mortgage lender. A survey of 2,863 UK residents conducted by TLF on behalf of the mortgage broker also found that 58% of respondents […]]]>A new study from Boon Brokers has discovered that 83% of people across the country are unaware of certain activity on their bank statements, which could be a red flag for a mortgage lender.

A survey of 2,863 UK residents conducted by TLF on behalf of the mortgage broker also found that 58% of respondents had never considered gambling transactions on their account to cause problems.

One in two people (47%) have gambled in the past month, but many don’t know that doing so could jeopardize their chances of getting a good mortgage.

When given a list of transactions that might give lenders reason to take a closer look, 55% didn’t think payday loans would be a cause for concern, and 58% didn’t. considered being constantly exposed to be a red flag.

According to Boon Brokers, three in four (72%) didn’t think having multiple payouts without a clear reference to their usefulness would raise alarm bells.

Gerard Boon, Partner at Boon Brokers, said: “Not all lenders will scrutinize your bank statements, but if you are considered a higher risk, perhaps with a smaller deposit or as a self-employed lender, lenders are more likely to take a closer look. Anything that shows the account holder may be having trouble getting into debt or controlling spending is likely to create questions.

He continued: “Our research revealed that the equivalent of 1.38 million current homeowners would consider trying to hide transactions on their bank statement to ensure their mortgage was approved – which we would not recommend. certainly not.

“If you’re considering applying for a mortgage or remortgage within the next six months, it’s worth being aware of which may lead to further inquiries – although in many cases it’s completely harmless. and easy to explain.”

He added that this could lead to unnecessary delays in your mortgage application, which could prevent you from getting the property you want.

However, not all things that could cause a problem are as easily identified as gambling, payday loans or overdraft, but there are others as well.

Boon Brokers’ research found that deals people were least likely to know about could be red flags for a mortgage lender.

Work for a family business

Only three percent of people realized this could be a problem. Lenders may suspect that a family member employed a relative for the purpose of getting a mortgage.

Using rude or joking references for payments to family and friends

Only one in 10 (9%) said they thought it might delay a mortgage application, but using ‘funny’ references that could be misinterpreted can mean a lender needs to investigate further.

(Image: Getty Images)

Have multiple payments for luxury items

Only nine percent thought it might be a potential concern. Lenders will worry if they feel the expenses are out of control and beyond what they would expect based on the applicant’s income

Have a lot of PayPal transactions

While PayPal transactions themselves aren’t a problem, as it’s not always clear who is being paid, having a lot of vague PayPal transactions can raise concerns.

Catalog or on payment on credit

Buy now, pay later options can signal to a lender that you are unable to prepay for common items or that you are buying things beyond your means – which only 13% of people have achieved.

play bingo

Playing once in a while for fun with friends won’t be a problem, but a regular habit with larger sums could be classified as gambling, which can raise a red flag.

Multiple store cards

Store cards by themselves aren’t a problem, but if you’re struggling to pay off the balance each month, given their notoriously high interest rate, it could be a warning sign for the lender.

Frequent payments to unknown third parties

There are many obvious reasons for making frequent third-party payments, but whenever possible, it’s best to spell out the reason to minimize any risk of red flags.

Large cash deposits or cashier work

Surprisingly, only 20% of people thought this would be of interest to a mortgage lender, who will want to see proof of a stable, reliable and legitimate income.

Take out a recent credit card

Only one in five (22%) have realized that applying for new credit can cause your credit score to drop, something all lenders will look at to assess your eligibility.

To read the 15 red flags that could affect your mortgage application, visit the Boon Brokers website here.

Get the latest savings and benefits news straight to your inbox. Sign up for our weekly Money newsletter here.

Advertising is undergoing a fundamental shift from traditional mediums to programmatic, omnichannel and digital formats. Digital advertising encompasses mobile ads, connected television (CTV), video, search, and more. The trading post (NASDAQ: TTD) operates on the demand side of the equation, working with advertisers and their agencies. PubMatic (NASDAQ: PUBM) occupies the sales side, working with […]]]>

Advertising is undergoing a fundamental shift from traditional mediums to programmatic, omnichannel and digital formats. Digital advertising encompasses mobile ads, connected television (CTV), video, search, and more. The trading post (NASDAQ: TTD) operates on the demand side of the equation, working with advertisers and their agencies. PubMatic (NASDAQ: PUBM) occupies the sales side, working with […]]]> [ad_1] smshoot / iStock via Getty Images introduction It appears that the butchering of stock prices for high growth stocks continues so far into 2022 and, as Sea (NYSE: SE) has been immune for quite a while, over the last few weeks that has changed as well. The stock is now trading down 49% from […]]]>

[ad_1] smshoot / iStock via Getty Images introduction It appears that the butchering of stock prices for high growth stocks continues so far into 2022 and, as Sea (NYSE: SE) has been immune for quite a while, over the last few weeks that has changed as well. The stock is now trading down 49% from […]]]>

[ad_1] Holdings reached (NASDAQ: UPST) caused a stir in 2021, entering markets in December 2020 with a moderate start before climbing over 750% in October 2021. Excitement cooled, but fintech stock still gained around 280% for the year. Management’s expectations for 2022 are also dampening some enthusiasm. What should investors do this year? To buy? […]]]>

[ad_1] Holdings reached (NASDAQ: UPST) caused a stir in 2021, entering markets in December 2020 with a moderate start before climbing over 750% in October 2021. Excitement cooled, but fintech stock still gained around 280% for the year. Management’s expectations for 2022 are also dampening some enthusiasm. What should investors do this year? To buy? […]]]>

[ad_1] Text size A man walks past an Alibaba sign outside the company’s Beijing offices. Greg Baker / AFP via Getty Images Ali Baba and other US-listed Chinese tech giants traded lower on Friday, but only after surging in the previous session in an attempt to rebound from a difficult year. Alibaba (ticker: BABA) fell […]]]>

[ad_1] Text size A man walks past an Alibaba sign outside the company’s Beijing offices. Greg Baker / AFP via Getty Images Ali Baba and other US-listed Chinese tech giants traded lower on Friday, but only after surging in the previous session in an attempt to rebound from a difficult year. Alibaba (ticker: BABA) fell […]]]>