Spencer Platt/Getty Images News

The Travelers Companies, Inc. (NYSE:TRV) is one of the largest P&C insurance companies in the country. Although the P&C insurance industry is highly fragmented and competitive, its unique nature allows insurers to realize economic benefits. The industry has shown positive results despite struggling with a return from non-catastrophic losses to pre-pandemic losses. Travelers is an elite player in the industry, with healthy underwriting profits and investment income providing the foundation for creating shareholder value. Management’s interests are aligned with those of investors and they have returned money to investors in the form of dividends and share buybacks at aggressive rates. Travelers’ free cash flow is substantial and supports the company’s dividend and stock buyback program. Free cash flow is also undervalued, as well as the company as a whole.

Insurance: where competition does not harm profitability

Peter Thiel rightly argues that “competition is for losers”. Competition pushes returns toward the cost of capital, making it difficult, if not impossible, to create economic value. At first glance, the insurance industry should be a very unprofitable industry. According to the National Association of Insurance Commissioners (NAIC), Travelers is the sixth largest P&C insurance company in the United States, with just 3.96% market share. The insurance industry is highly fragmented. The NAIC’s 2020 Market Share Report lists 125 leading P&C insurers offering products and services across all lines.

Source: NAIC

Among travelers Filing 10-K 2021, they cite statistics from AM Best showing that there are about 1,100 P&C insurance groups in the United States, comprising about 2,600 P&C insurance companies. In 2020, the top 150 insurers account for around 94% of the sector’s total net premiums written. If competition is for losers, then on the face of it, the insurance industry is an industry of losers.

However, the insurance sector is unique. Insurance is required by law, so the business tends to be relatively stable. Regardless of the economic cycle, individuals and businesses need insurance. This gives insurers pricing power that they would not otherwise have.

Insurance products lack real differentiation. Success is earned through a combination of agent referrals, cost, and brand awareness. Agent referrals are important because most people get their insurance through an agent. Insurers need agents to run business as they please. Because differentiation doesn’t really exist, insurers need to be able to price their products at lower rates than their competitors. Brand awareness is important because insurance is about trust and strong brands tell consumers they can trust the insurer.

P&C insurance recovers from the pandemic

The sector posted good premium growth and strong financial results in 2021, despite the disruptions the sector has suffered.

The industry has accelerated its adoption of new technologies, spurred by the pandemic and the need to adapt to supply chain disruptions. These innovations aim to help insurers improve their pricing policies, improve their efficiency and reduce their costs.

According to Aon (NYSE: AON), total premium growth in the first nine months of the year was 9.5%, up 7.3 points from the same period in 2020. Commercial lines increased by 9.8 %, compared to personal lines which increased by 4.8%. As the economy recovered, the sector also saw growth in commercial and personal autos as well as workers’ compensation. Travelers is the market leader in workers’ compensation, with 6.84% of the market. It is also the second largest insurer in total commercial auto, with a market share of 6.22%. It is the tenth largest passenger car insurer overall, with a market share of 1.96%.

The industry has experienced a Net underwriting loss of $5.6 billion due to a return of non-catastrophic losses to pre-pandemic levels. However, the industry’s net income grew 8% in the first nine months of 2021, from $35.5 billion in 2020 to $43.5 billion in 2021, fueling surplus growth. 73% politics. The total expense ratio remained at 38.4%.

Aon’s reports also show that direct loss ratios across most lines in the first nine months of 2021 were lower than in the same period a year earlier.

Source: Aon

The path to profitability

According to Travelers Fourth Quarter 2021 Results, in 2021, Travelers had a loss and loss adjustment ratio of 65.1%, unchanged from 2021, and an underwriting expense ratio of 29.4%, compared to 29.9% in 2020, for a combined ratio of 94.5% compared to 95% the previous year. As an indication, according to a report from Veriskthe P&C insurance industry had a combined ratio of 99.5% in the first nine months of 2021.

An insurer derives its income from its underwriting and investment activities. Premiums paid by policyholders constitute a float that insurers can use to invest. Underwriting profits arise when the insurer receives more in premiums than it pays in claims.

Travelers earns a profit from its underwriting activities and invests those profits in a portfolio consisting largely of fixed income instruments. Travelers has grown its premiums from more than $28 billion in 2018 to nearly $30.9 billion in 2021. During this period, net investment income has grown from approximately $2.5 billion to over $3 billion.

The company’s combined ratio reflects the profitability of the business and its technical margin of 5.5%.

The company’s underlying combined ratio, which represents fewer catastrophic losses, was 90.3%, showing that the company’s editorial was particularly good, having improved an already impressive underlying combined ratio of 90.7% the previous year.

The interests of management are aligned with those of shareholders

The company’s 2004 incentive plan resulted in a performance share reward program. Under this program, performance share grants are linked to the achievement of an adjusted return on equity (ROE) over a three-year period. When management does not achieve these objectives, it cannot acquire performance shares. When he reaches or exceeds these objectives, a range of performance shares is acquired (50% to 150% for grants in 2020, 50% to 200% for grants in 2021 and 2022), depending on the ROE achieved. .

Although ROE is an imperfect measure, and I prefer return on invested capital (ROIC), it is useful for aligning the interests of management with those of shareholders. By doing so, shareholders know that management will make decisions that will create value for the company, or at least aim to do so.

The History of Traveler Profitability

Travelers increased its revenue from $27.6 billion in 2016 to $34.2 billion in 2021. During this period, it increased its net operating income after taxes (NOPAT) by nearly 2.9 billion to nearly $3.6 billion.

Source: Documents filed by the company and calculations by the author

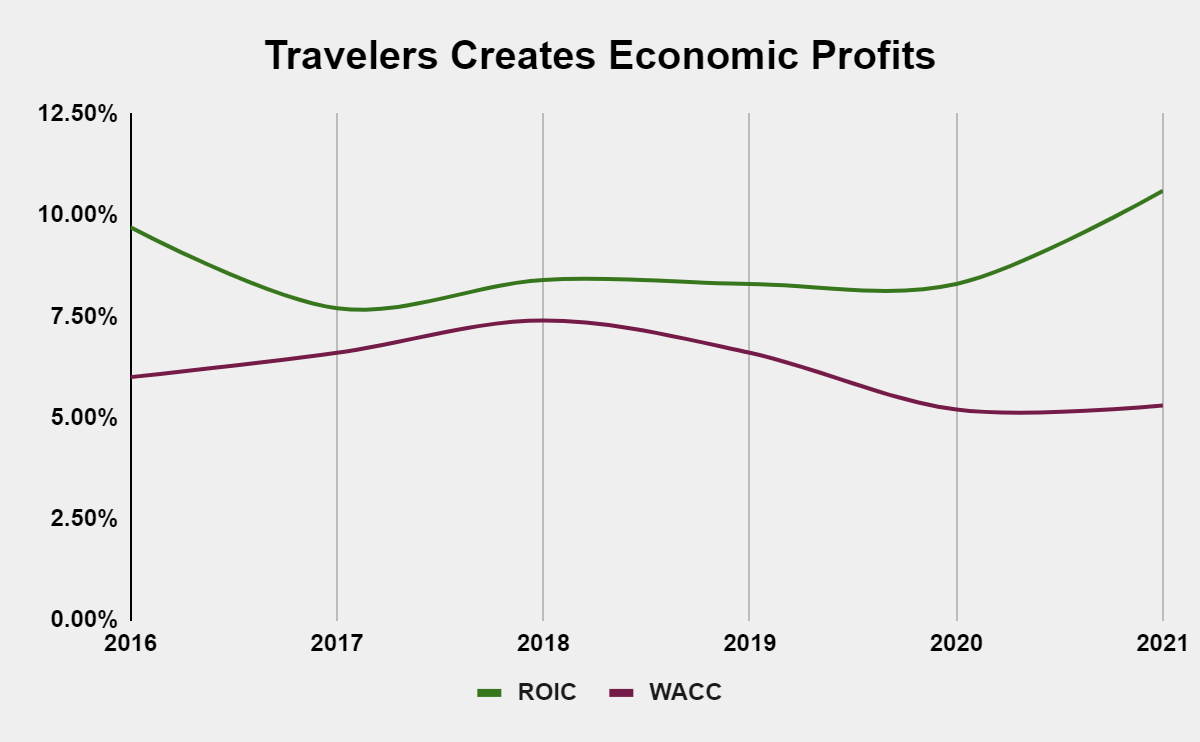

Travelers’ NOPAT margin was 10.4% in 2016, falling to 7.9% in 2017, averaging 8.15% between 2017 and 2020, before returning to 10.4% in 2021. The results show an invested capital turnover of 1.02, showing excellent capital allocation efficiency. The combination of these two elements resulted in an improvement in ROIC from 9.7% in 2016 to 10.6% in 2021.

Source: Company filings, author’s calculations

The profitability of travelers allows it to generate significant free cash flow (FCF). However, FCF has been erratic, growing from nearly $2.8 billion in 2016 to over $1.8 billion in 2021, for a cumulative FCF of over $10.4 billion, or 25% of its market capitalization.

Source: Documents filed by the company and calculations by the author

Travelers’ ability to generate substantial FCF has enabled it to increase its common stock dividends for each of the last 18 yearsfrom $1.16 in 2004 to $3.49 in 2021.

The company’s FCF has always been attractively priced, which speaks to the company’s overall state of undervaluation. Significant FCF generation and attractive pricing suggest the company’s economics are strong and future stock price performance will be good. Currently, the company has an attractive FCF yield of 4.2%.

Travelers has a generous dividend payout ratio of 24.24%, which reflects its ability to grow without major investments. The company’s FCF can support the company’s dividend policy, which currently yields 2.04%. In April 2021, the company implemented a stock repurchase authorization that added $5 billion in repurchase capacity. In 2021, Travelers repurchased 13.9 million shares under its $2.16 billion stock repurchase authorization. As of December 31, 2021, Travelers’ had $4.01 billion of capacity remaining under its stock repurchase authorization.

Evaluation

Not only is the company’s FCF attractively priced, but the company itself is undervalued. Travelers has a price/earnings ratio (P/E) of 11.77 and a 5-year P/E ratio of 14.11. In comparison, the S&P 500 has a P/E ratio of 24.87. The implication is not only that investors can buy the company at an attractive price, but that shareholders can also earn attractive returns from this same undervaluation.

Conclusion

Industry effects govern a firm’s ability to sustainably earn economic profits. Despite the competitive nature of the P&C insurance industry, the fact that it is both broadly mandated by law and essential to mitigating the risk of economic loss, makes the industry not only non-cyclical, but one in which rivals can achieve economic benefits. . Additionally, the insurance sector showed signs of recovery, despite the disruptions in the sector, as non-catastrophic losses returned to pre-pandemic levels. The result is that Travelers operates in a favorable competitive landscape. In this landscape, the company has shown its ability to grow profitably and generate returns above the opportunity cost of capital. The insurer’s profitability enables it to generate free cash flow, the price of which has been attractive on the market. Additionally, the company remains undervalued relative to the broader market, making it a very attractive stock to buy.

Comments are closed.